What Happens If a Housing Association (Registered Provider) Fails? An Investor’s Guide to Social Housing Risks

Why the social housing sector is designed to protect homes, tenants and long-term investors.

Don’t invest unless you’re prepared to lose money. This is a high-risk investment. You may not be able to access your money easily and are unlikely to be protected if something goes wrong. Take 2 mins to learn more.

Don’t invest unless you’re prepared to lose money. This is a high-risk investment. You may not be able to access your money easily and are unlikely to be protected if something goes wrong. Take 2 mins to learn more.

Why the social housing sector is designed to protect homes, tenants and long-term investors.

Launched on the Exchange in 2021, Abingdon Way is bungalow with a strong yield in partnership with Golden lane Housing

How does our proprietary, multi-factor risk framework operate, and how does it evaluate the fine margins of our risk spectrum?

Driven by a decades-long government policy shift away from institutional care toward community-based independent living, supported housing has transitioned into a highly sophisticated, institutional-grade asset class.

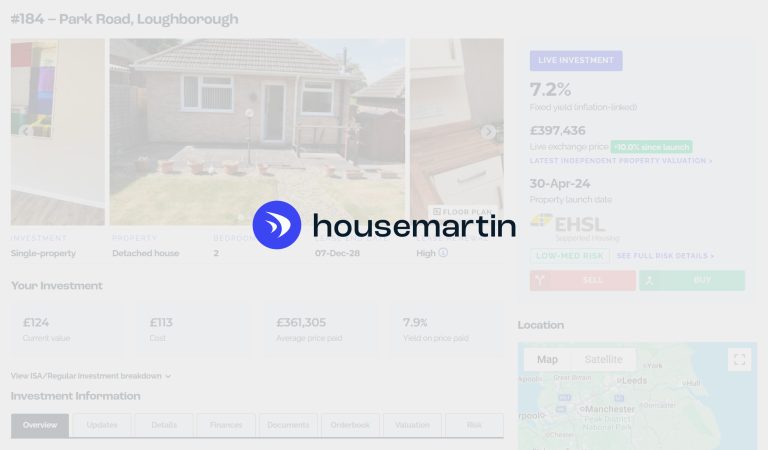

We’ve just updated the Property details page to make the information easier to read, while keeping the same depth of detail.

Cumbria Quality Care focuses on supporting people with complex needs, including autism, learning disabilities and other conditions requiring high levels of specialist support.

For investors hoping the UK had finally turned the corner on the cost-of-living crisis, the announcement that the Ofgem energy price cap will rise by a staggering 13% this July delivers a sobering reality check.

Launched on the exchange in 2021, our property on Tewther Road offers a strong yield in a partnership with Nacro.

How are these schemes actually funded and where does the real risk sit?

Stay up-to-date with the latest insights and property announcements